Nebius Group N.V. (NBIS) - Deep Dive

There are very few companies in the public markets that have gone from essentially zero revenue to a $20 billion contractual backlog in 18 months, and Nebius is one of them.

Nebius Group N.V. (NASDAQ: NBIS) builds and operates large-scale GPU clusters, cloud platforms, and developer tools for the global AI market, renting compute capacity to AI developers, enterprises, and hyperscalers under both on-demand and long-term contract arrangements. The core AI cloud business represents roughly 90% of group revenue.

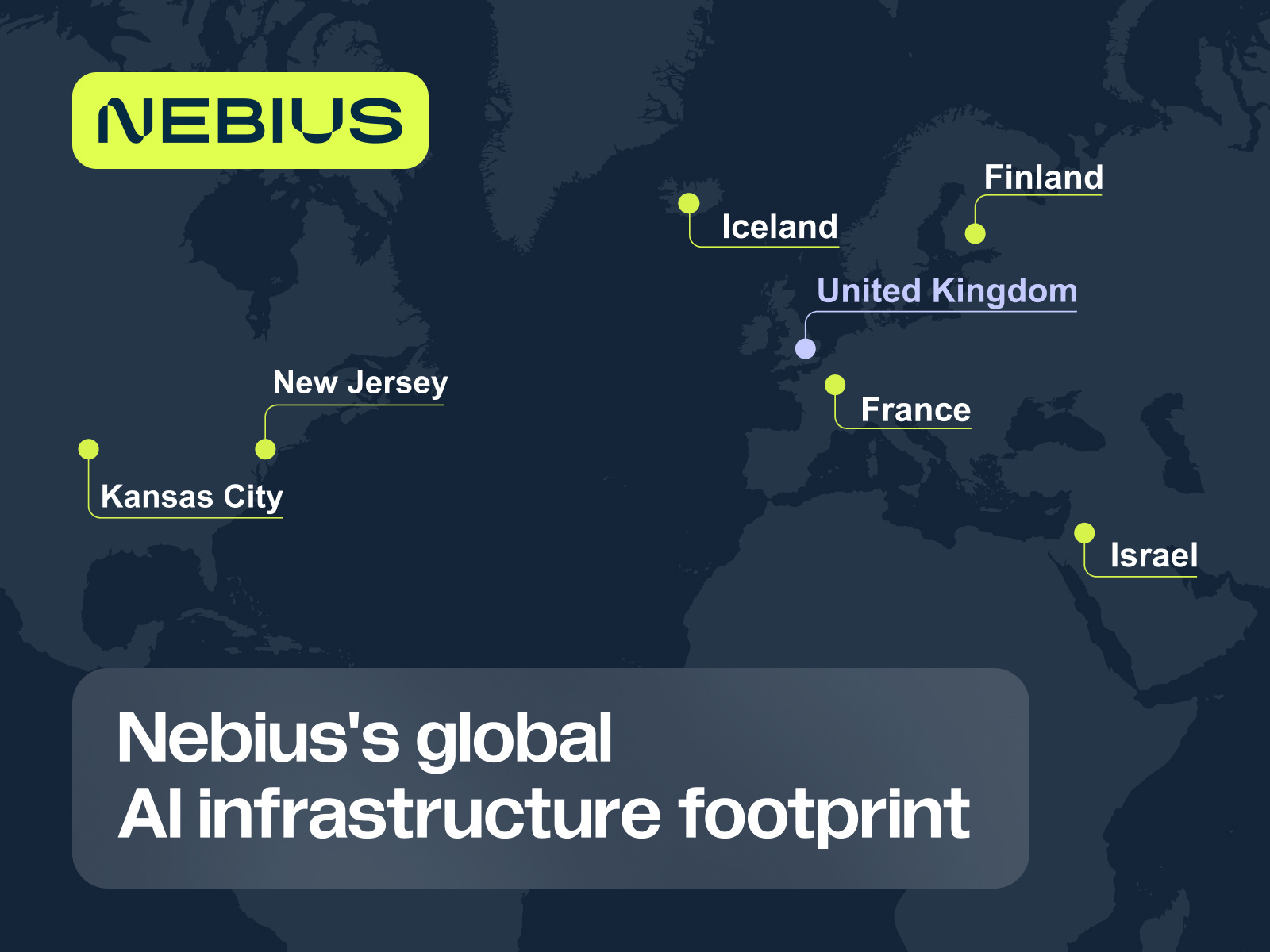

Headquartered in Amsterdam and listed on Nasdaq, Nebius operates data centers across Finland, France, Iceland, the United Kingdom, the United States, and Israel, with contracted power capacity exceeding 2 gigawatts (GW) as of February 2026 and a target of more than 3 GW by year-end.

Nebius used to be called Yandex N.V., the Dutch parent of Russia’s dominant search conglomerate. Following the 2022 Ukraine invasion, the company divested all Russian operations in a $5.4 billion transaction and relaunched in October 2024 with co-founder Arkady Volozh returning as CEO, a clean slate, and a serious engineering workforce inherited from one of Europe’s most capable technology companies.

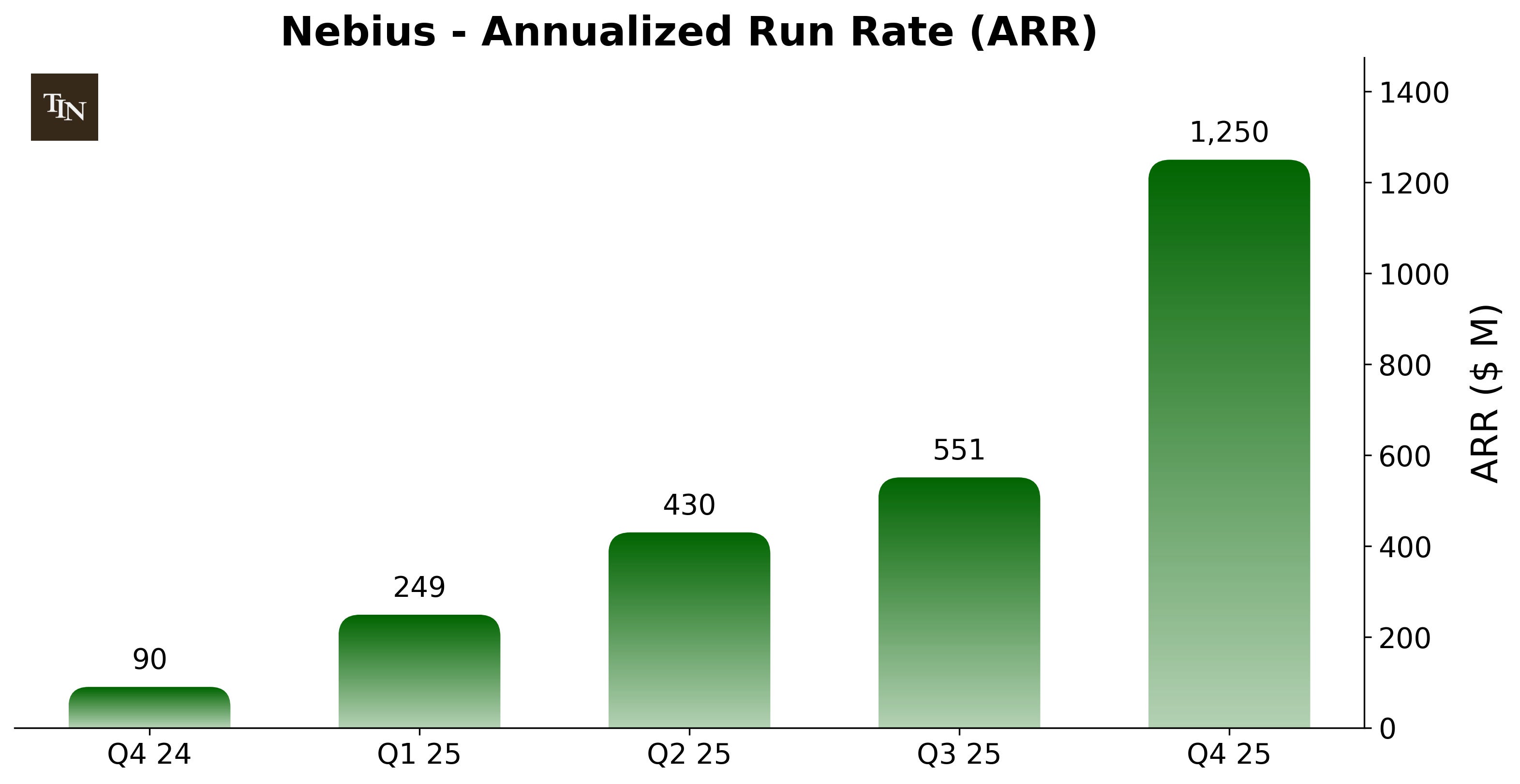

Revenue has since scaled exponentially, from $117.5 million in 2024 to $530 million in 2025, $228 million of which in Q4 2025 alone, representing 547% year-over-year growth in that quarter. The company exited 2025 with annualized run-rate revenue (ARR) of $1.25 billion, above its own guidance, and is targeting $7-$9 billion ARR by December 2026.

Beyond the core AI cloud, the group includes Toloka (AI training data), Avride (autonomous vehicles), and TripleTen (edtech).

Practical Scenario

Imagine an AI startup that has built a promising image generation model and needs to train a next-generation version on hundreds of billions of data points. The job requires thousands of high-end NVIDIA GPUs running simultaneously for weeks. Building that infrastructure in-house would take years and cost hundreds of millions of dollars, and renting is the only economically viable alternative.

The startup visits Nebius’s cloud platform and selects a pre-configured GPU cluster. Using Nebius’s console or API, the team provisions resources in minutes. Nebius handles node orchestration via managed Kubernetes or Slurm, automated failure recovery, and proactive health monitoring (all built in-house rather than licensed from third parties). The startup pays on an hourly or reserved-capacity basis, with discounts for multi-month commitments. As the startup scales from hundreds of GPUs to tens of thousands, Nebius scales the cluster without any platform migration.

Revenue begins the moment the cluster is active, with the management calling this the “token factory” model. Capacity is sold before it is deployed, often with upfront prepayments from enterprise and hyperscaler clients who need guaranteed compute access. For example, in Q4 2025, operating cash flow reached $834 million against GAAP revenue of $228 million, where the difference reflects prepayments under multi-year agreements, most prominently Microsoft’s $17.4 billion, five-year commitment for capacity at Nebius’s Vineland, New Jersey facility. The business generates cash before it recognizes revenue, which is a sign of strong contractual positioning.

The Key Metric

The metric to track for Nebius is Annualized Run-Rate (ARR) Revenue, defined as the last month of a quarter’s revenue multiplied by twelve.

This matters more than reported quarterly revenue because Nebius is in an infrastructure ramp where capacity comes online in discrete steps. A new data center tranche that goes live in December contributes only one month of revenue to Q4, but will generate that monthly rate for all of the following year. ARR strips out this timing distortion and shows where the business is actually running at any given moment.

Tracking ARR alongside contracted power capacity (the pipeline indicator) and connected capacity (the live indicator) gives the most complete view of whether the buildout is on schedule.

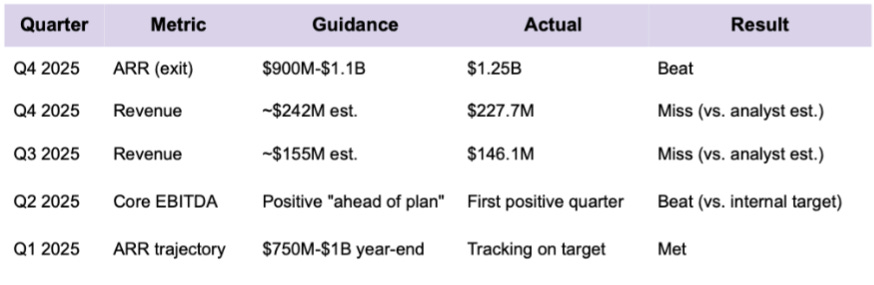

Management guides to ARR targets for exactly this reason, and the company has consistently beaten or met those targets since its October 2024 relaunch. When quarterly revenue misses analyst estimates, it is almost always an ARR beat in disguise, i.e., a capacity tranche deployed later in the quarter than modeled.

Why This Opportunity Might Exist

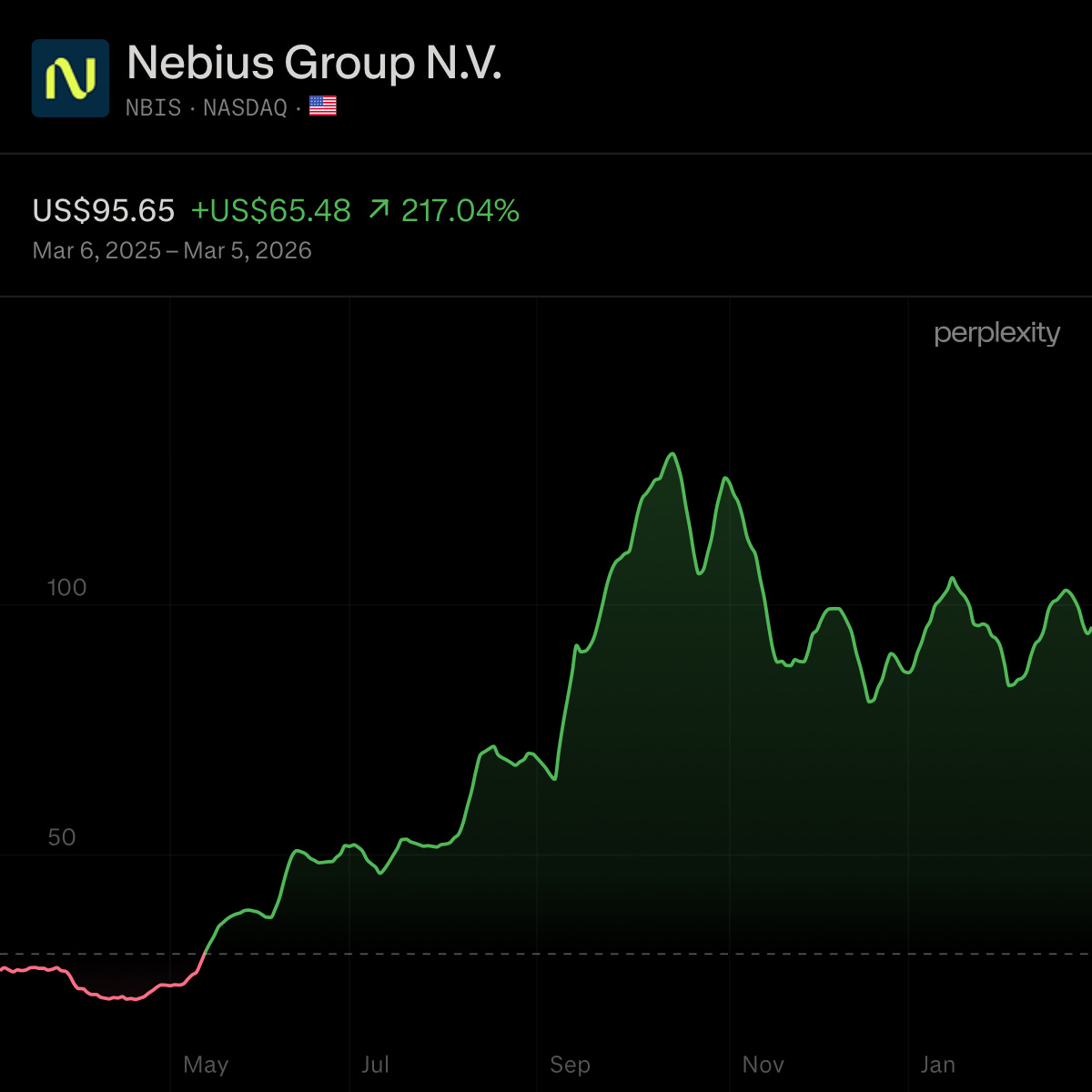

Analyst consensus currently remains decisively bullish, with consensus price targets average approximately $151 (range: $108-$232), implying roughly 55% upside from $97.78 (March 4 2026 close). The 52-week range runs from $18.31 to $141.10, leaving the stock approximately 32% below its October 2025 peak.

Bears focus largely on four concerns:

the trailing EV/Sales multiple prices in substantial 2026 execution on a capital program never attempted at this speed

Microsoft concentration is existential because the entire 2026 capacity buildout is sized against that single relationship

Yandex origins create friction in regulated enterprise markets

The neocloud model may structurally narrow as hyperscalers build AI-specific capacity in-house through 2027-2028.

The potential mispricing lies in the measurement frame. TTM revenue of $530 million is the wrong anchor. Contracted backlog exceeds $20 billion and ARR exited 2025 at $1.25 billion, already 2.4x trailing revenue. Forward EV/Sales on 2026 guidance of $3.0-$3.4 billion compresses to roughly 6-7x at current prices, which is a materially different valuation conversation.

Sentiment could shift substantially if the company demonstrates on-schedule capacity deployment through H1 2026 and shows enterprise diversification beyond its two current hyperscaler contracts.

Implications for Thesis

The most material development of the past twelve months is not the Microsoft contract itself but what it reveals about Nebius’s technical positioning. A hyperscaler with essentially unlimited internal capital chose to purchase $17-$19 billion of GPU infrastructure from an 18 month old neocloud because it could deliver training performance at scale that Azure struggled to guarantee internally.

That is the clearest possible validation of Nebius’s engineering differentiation argument, and with the subsequent Meta contract confirming that hyperscalers are deliberately splitting workloads across multiple neoclouds suggesting a structurally supportive dynamic for Nebius’s 2026 pipeline beyond the two named customers.

CoreWeave’s Q4 2025 earnings report (February 26) adds an important new data point to the execution risk argument. The Q1 2026 guidance miss — $1.9-$2.0 billion against a $2.29 billion consensus — triggered a 21% single-day decline and a further ~28% total drawdown over the subsequent week, demonstrating once again how severely the market penalizes neocloud guidance misses at high valuations.

Nebius fell 15% in sympathy on no company-specific news, which is itself informative of the fact that the sector trades as a single risk-on/risk-off trade when volatility spikes. This dynamic has two implications for Nebius specifically. First, the CoreWeave guidance cut confirms that execution slippage at this scale of buildout is not a tail risk but a base expectation, meaning that these are to be expected. Second, a Nebius guidance miss in Q1 or Q2 2026 would likely produce a comparable or worse stock reaction given Nebius’s even higher forward multiple.

The Tavily acquisition at $275 million upfront (up to $400 million with milestones) and the Missouri AI factory approval are two new data points that both pull in the same strategic direction. Nebius is building toward a full-stack position rather than remaining a pure GPU rental business, and it is securing power capacity in the United States at a scale that goes well beyond the current Microsoft buildout.

The Missouri campus at up to 1.2 GW represents a generational infrastructure commitment that won’t contribute revenue until H2 2026 at the earliest, but it meaningfully de-risks the concentration question by establishing Nebius’s largest U.S. presence independent of any single contract relationship. Meanwhile, the Tavily acquisition’s signals that the management team believes the platform’s long-term defensibility depends on owning the software layers above raw compute. The degree to which non-hyperscaler enterprise revenue grows as a share of total through 2026 remains the underappreciated metric to watch alongside ARR.

MANAGEMENT

CEO Profile

Arkady Volozh is the right person for this specific moment in Nebius’s development. He co-founded Yandex in 1997 and served as CEO through 2022, scaling it from a Russian search engine into a $30 billion diversified technology conglomerate that competed with Google on its home turf. That is a direct analogue for what Nebius needs to accomplish by building technically demanding, capital-intensive infrastructure at massive scale from a position of initial disadvantage against larger incumbents.

He relocated to Israel in 2014, publicly condemned the Ukraine invasion in August 2023, and executed the $5.4 billion Yandex Russia divestiture. His strategic instinct is reflected in the mid-year 2025 decision to raise 2025 CapEx guidance from $2 billion to $5 billion when hyperscaler demand became clear. The vision he articulates, “everything we build, we sell,” reflects a demand environment that has consistently outpaced the company’s ability to deploy capacity.

Key Executives

The two capability requirements most critical to Nebius’s current stage are institutional-scale financial management and enterprise revenue diversification. The existing leadership team addresses both directly. Maria “Dado” Alonso Sanchez(CFO), with prior experience at Amazon, Booking.com, and Naspers, brings institutional capital markets depth that is directly relevant as Nebius navigates multi-billion-dollar equity raises, $4.1 billion in convertible debt, and the financial complexity of a business where operating cash flow substantially exceeds GAAP revenue recognition. Marc Boroditsky(CRO), who grew Twilio’s customer base sixfold and revenue more than tenfold to $4 billion at his prior role, was hired explicitly to address Nebius’s most critical medium-term challenge: building non-hyperscaler enterprise revenue before the Microsoft buildout phase transitions to steady-state. Ofir Nave (COO) oversees the multi-continent data center footprint at the exact moment when operational execution is the single largest risk variable in the business.

Insider Ownership & Activity

Volozh directly owns approximately 12.23% of shares outstanding, worth approximately $2.2 billion as of early March 2026. That level of founder concentration is a genuine alignment signal, a CEO whose personal wealth is tied to the company’s success has every incentive to make decisions in shareholders’ long-term interest. Form 144 filings show Volozh executed discretionary sales between July and September 2025, including a single transaction of approximately 2,048,975 shares generating roughly $187.9 million in gross proceeds. This represents a personal portfolio diversification executed into a rising stock following the Microsoft announcement, and Volozh’s retained position remains the single largest individual stake in the company by a significant margin.

COMPETITIVE POSITION

Competitive Position & Moat

Nebius operates in the “neocloud” segment, specialized providers focused exclusively on high-performance GPU compute for AI training and inference, as distinct from general-purpose hyperscalers. The industry is in a land-grab phase where AI model complexity is growing faster than any single company’s ability to build capacity. Nebius has been sold out every quarter since scaling began, and Q1 2026 is already fully committed. Scarcity is the dominant competitive dynamic, and it is a favorable one for the current holders of infrastructure.

The company’s competitive position rests on four interlocking factors with varying durability.

Vertical integration is Nebius’s most distinctive technical advantage. Rather than reselling commodity GPU capacity from standard rack configurations, Nebius designs its own server chassis, racks, and networking software, optimizing specifically for the latency and throughput demands of large-scale AI training. The company operates ISEG, ranked among the world’s twenty most powerful supercomputers by top500.org, at its Finland facility, evidence of engineering capability well beyond what a standard cloud reseller can deliver.

Training a large AI model requires thousands of GPUs to communicate synchronously, and any networking inefficiency compounds across the cluster. Nebius’s custom InfiniBand configuration enormously reduces that latency. Microsoft’s decision to source infrastructure from Nebius is the most credible third-party validation of this advantage available.Platform switching costs are real but still developing. Nebius has expanded beyond raw GPU rental into a full-stack platform including managed Kubernetes and Slurm clusters, proprietary storage, AI Studio with 60,000+ registered users, enterprise-grade security certifications (SOC 2 Type II, HIPAA, ISO 27001), and the Tavily agentic search acquisition.

As customers integrate their training workflows, data pipelines, and inference infrastructure into Nebius’s managed services, migration to a competitor becomes progressively more disruptive. Q4 2025 showed nearly twice as many contracts exceeding twelve months compared to Q3, with average selling prices rising more than 50%, which is consistent with customers paying a premium for the integrated platform rather than simply buying the cheapest available GPU hours.Contracted power is a genuinely durable infrastructure moat, and possibly the most underappreciated one. In the neocloud business, power capacity is more constraining than GPU availability. Nebius has over 2 GW of contracted power as of February 2026, targeting 3+ GW by year-end. The Independence, Missouri campus approval adds a further 1.2 GW of potential future capacity. Replicating this position would take a new entrant at least 18-36 months of permitting, grid interconnection negotiations, and construction commitments, regardless of how much capital they raise. That window gives Nebius meaningful protection from capital-flush new competition over the next two to three years.

NVIDIA’s equity stake (approximately 0.5%) and NVIDIA Cloud Partner designation provide preferential GPU allocation, Blackwell B200, B300, and GB300 NVL72 systems. Nebius was among the first providers to deploy Blackwell Ultra and was named a launch partner for NVIDIA Dynamo and Vera Rubin. NVIDIA also holds equity in CoreWeave, so this advantage is shared rather than exclusive, but first-deployer status on successive hardware generations is a signal that the relationship is substantive.

IDC projects AI infrastructure spending exceeding $758 billion by 2029 at a 42% CAGR for accelerated servers. The GPU-as-a-Service segment that Nebius primarily occupies is projected to reach $27-$50 billion by 2030. More than 100 neocloud providers exist globally, but the set of companies with substantial contracted power, hyperscaler relationships, and sufficient capital to compete is narrow, and narrowing.

Key Competitors

CoreWeave (NASDAQ: CRWV) is the neocloud market leader by scale, with full-year 2025 revenue of $5.1 billion against Nebius’s $530 million, a revenue backlog of $66.8 billion, and a Q4 2025 earnings report (released February 26, 2026) that beat revenue estimates at $1.57 billion but guided Q1 2026 revenue of $1.9-$2.0 billion against a $2.29 billion consensus, sending the stock down approximately 21% on the day and roughly 28% over the subsequent week to around $74.

The structural weakness of the company is primarily financial. CoreWeave carries approximately $21-$30 billion in total debt and lease obligations with interest expense tripling year-over-year, a capital structure that requires perfect execution and sustained contract conversion to remain viable. Nebius has a cleaner balance sheet and meaningfully lower leverage, but far less proven scale.

Lambda Labs is a private, NVIDIA-backed neocloud targeting cost-conscious AI researchers and startups. The company competes primarily on price with one-click GPU cluster deployments and simplified onboarding. Lambda occupies the opposite end of the neocloud spectrum from Nebius: low complexity, low switching costs, lower price point. Its primary weakness relative to Nebius is the absence of the managed services, enterprise compliance certifications, and developer ecosystem that enable Nebius to serve hyperscaler and regulated-industry clients. Lambda’s trajectory is stable but not accelerating at Nebius’s pace.

AWS, Azure, and Google Cloud are simultaneously Nebius’s most important near-term customer relationship and its most significant long-term competitive threat. Microsoft Azure signed a $17.4-$19.4 billion contract with Nebius because Azure was supply-constrained, a situation that validates Nebius’s technical quality while revealing the uncomfortable dynamic where its largest customer is also the entity most likely to reduce demand if it successfully builds sufficient AI-specific compute in-house. The hyperscalers collectively dominate 63%+ of the cloud market and are spending hundreds of billions on AI infrastructure.

Competitive Position Score: 18/30

BUSINESS QUALITY

Revenue Engine & Key Metric

ARR, defined as the last month of the quarter’s revenue multiplied by twelve, as mentioned earlier, is the metric that actually tells you where Nebius business is headed. Reported quarterly revenue is a misleading signal because new data center tranches contribute only one month of revenue in their go-live quarter but the full monthly rate in every subsequent period. ARR strips out this timing artifact and captures the genuine exit velocity of the business.

The $1.25 billion ARR exit for 2025 versus management’s initial target of $750 million-$1 billion reflects a consistent pattern of conservative guidance followed by execution that matches or exceeds the high end. The 2026 ARR target of $7-$9 billion implies 5.8x-7.5x growth in a single year, driven by contracted capacity scaling from approximately 220 MW to 800 MW-1 GW of connected infrastructure.

The revenue structure of Nebius is primarily subscription-like, whereby customers sign long-term contracts (often 12+ months) with upfront prepayments, generating operating cash inflows that lead GAAP revenue recognition. The caveat is customer concentration. Microsoft alone represents the vast majority of contracted 2026 backlog. Meta’s $3 billion commitment has meaningfully diversified the mix, and management reports accelerating enterprise clients, but the concentration risk remains (discussed at length in Material Risks section).

Profitability & Capital Returns

Nebius remains pre-profitability on a GAAP basis, but the margin trajectory over the past four quarters makes a compelling argument that the economics of this business are genuinely attractive once infrastructure is deployed.

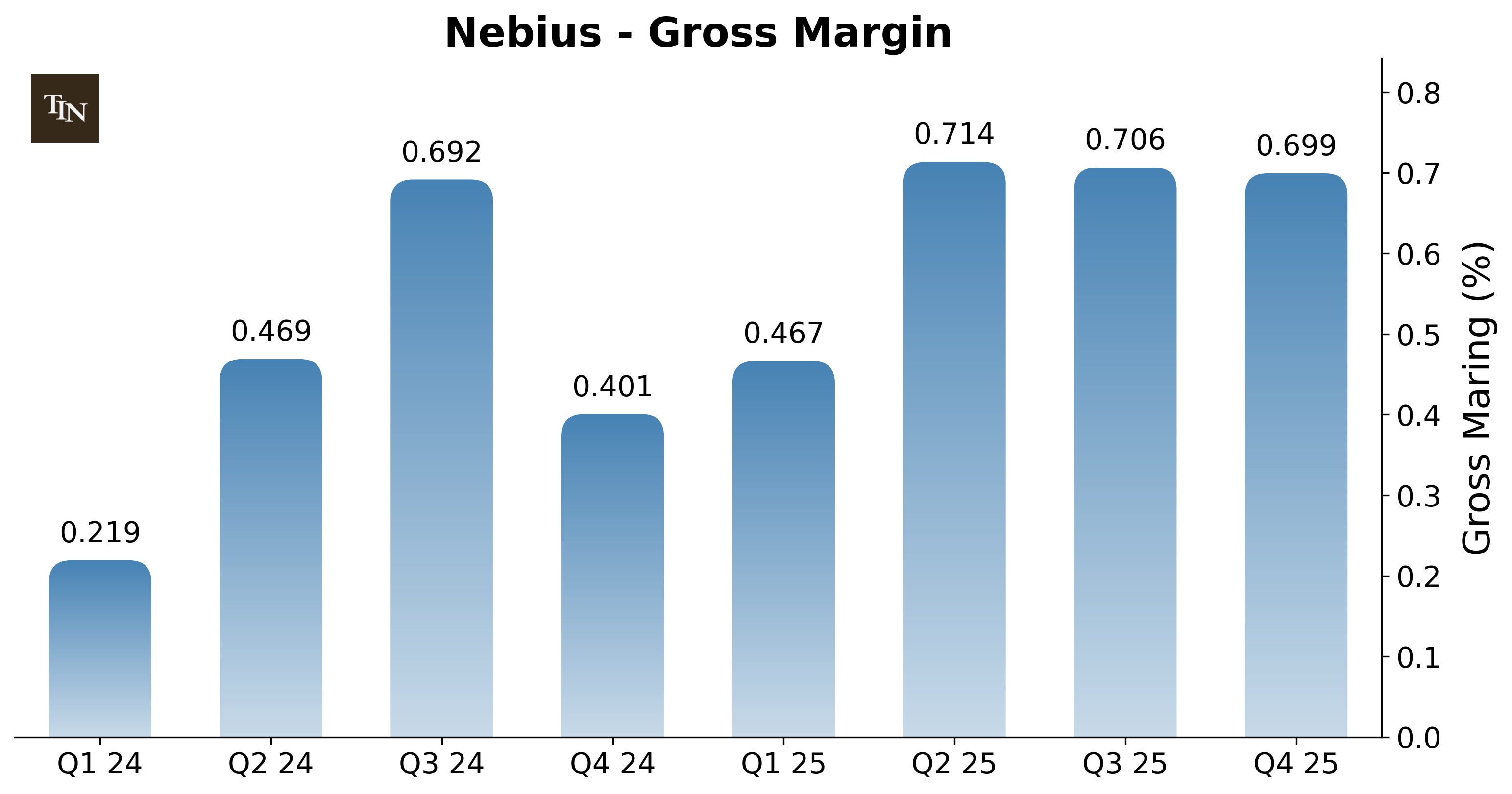

The ~70% gross margin in Q4 2025 is the number that deserves attention. GPU cloud businesses generate high gross margins because once infrastructure is procured and depreciated, incremental compute capacity carries very low variable cost. The margin improving from the low 60s to approximately 70% as Nebius scales reflects the operating leverage of filling contracted capacity at long-term rates, customers who have committed to multi-year contracts at premium pricing rather than competing on hourly spot rates.

For context, CoreWeave’s reported gross margin runs slightly higher at approximately 74% in Q4 2025. Nebius’s adjusted EBITDA Margin for the core business moved from negative throughout 2024 to a small positive in Q2 2025 to 19% in Q3 2025 and 24% in Q4 2025. Management is guiding for 40% adjusted EBITDA margin by end of 2026, a trajectory that looks credible given the pace of improvement.

ROIC and ROE are not meaningful given pre-GAAP-profitability, but full-year 2025 adjusted net losses narrowed from $266.4 million in FY2024 to $64.9 million in FY2025 on revenue that grew 479%, which is the operating leverage signal that matters.

Capital Deployment & Execution

Nebius’s capital story is uncomplicated in structure and staggering in scale. There are no material acquisitions beyond the Tavily tuck-in at $275 million ($400 million including milestones), no buybacks, and no dividends. Everything is going into infrastructure buildout. Q4 2025 capital expenditure alone was approximately $2.1 billion against $228 million of GAAP revenue, a ratio that would look alarming for almost any other business but is logical here because roughly 80% of that CapEx represents GPU procurement contracted against specific customer deals: the hardware is being purchased to fulfill the Microsoft and Meta agreements, not speculatively. Full-year 2025 CapEx was approximately $5 billion. The company ends 2025 with $3.68 billion in cash and $4.1 billion in non-current convertible debt, providing approximately two years of runway before additional financing is needed. Free Cash Flow was approximately negative $4.6 billion for FY2025, expected to remain deeply negative through the buildout phase as contracted prepayments from customers increasingly fund the CapEx cycle.

The R&D picture is embedded in operational costs: 1,000+ former Yandex engineers produce proprietary server chassis, custom networking software, AI Cloud 3.1, and AI Studio. Share count increased to 253,016,971 as of December 31, 2025, reflecting equity raises throughout the year.

The execution pattern here is easy to misread. The quarterly revenue misses look concerning until you understand what drives them: analysts repeatedly struggle to model the timing of capacity deployment, and new data center tranches that go live later in a quarter contribute one month of revenue rather than three. The company consistently beats its own internal ARR guidance, which is the metric management actually controls and emphasizes. Management has explicitly noted that analysts still don’t fully understand how to model this business. The ARR beats are what matter operationally.

Business Quality Score: 17/30

MARKET OPPORTUNITY & RISKS

Total Addressable Market

The GPU-as-a-Service (GPUaaS) market that Nebius primarily competes in was valued at approximately $5.8-$8.2 billion in 2025 and is projected to reach $26.6-$49.8 billion by 2030 at a CAGR of 26.5%-35.8% (Fortune Business Insights, 2025; MarketsandMarkets, 2025). IDC’s October 2025 tracker projects the broader AI infrastructure market reaching $758 billion by 2029 at a 42% CAGR for accelerated servers. Nebius’s 2025 revenue of $530 million represents roughly 6.5%-9.1% penetration of the GPUaaS market as currently sized, placing it firmly in the scaling phase with substantial runway ahead.

Geographic (contracted) expansion continues steadily, with Nebius currently building across the US, UK, Iceland, France, Israel, and Finland, positioning as one of the few neoclouds with credible European data sovereignty credentials at a moment when EU AI Act compliance requirements are tightening, which is a growing differentiator against US hyperscalers for European enterprise customers.

Enterprise vertical expansion is being enabled by the December 2025 AI Cloud 3.1 certification suite (SOC 2 Type II, HIPAA, ISO 27001), unlocking healthcare and financial services customers previously unable to use the platform. Finally, inference and agentic workloads open a structurally different, higher-margin revenue stream as AI moves from model-building to production deployment. AI Studio, Tracto.ai, and the Tavily acquisition all position Nebius to capture this shift.

Material Risks

The most pressing concern for the company is customer concentration, with Microsoft currently representing more than 80% of contracted 2026 backlog through the $17.4-$19.4 billion five-year agreement, and the 2026 capacity buildout is sized and financed against this one relationship. Loss or renegotiation of this contract would collapse the $7-$9 billion ARR target along with the entire investment thesis. Management is actively pursuing diversification, and Meta’s $3 billion commitment is the most meaningful progress to date, only limited by available capacity.

Operational and execution risk is the second category and the one hardest to underwrite from the outside. Nebius is attempting to scale from approximately 220 MW of connected capacity to 800 MW-1 GW within a single calendar year, a 4-5x expansion requiring simultaneous delivery across data center construction on three continents, GPU procurement at $15+ billion CapEx scale, regulatory approvals in multiple jurisdictions, and rapid workforce integration.

CoreWeave’s Q4 2025 earnings miss substantiate a failure that Nebius could face. The market’s tolerance for guidance misses in this sector is effectively zero given the valuation levels at which these stocks trade. NVIDIA Blackwell availability is globally constrained, and preferred partner status provides priority access but not immunity from production disruptions.

Geopolitical exposure remains latent despite sanctions being lifted. Nebius’s Yandex lineage creates reputational friction with the regulated-industry enterprise customers (financial services, defense, government) that represent the higher-margin segment Nebius needs to build toward. The EU AI Act and evolving US AI export controls could impose compliance costs or restrict specific workload types.

In the longer-term, the primary constraint for Nebius comes from competition. AWS, Azure, and Google have collectively planned over $300 billion in AI infrastructure investment in 2025, and as they build AI-specific compute at scale, the neocloud value proposition narrows to the specialized niches and geographies hyperscalers choose not to serve. If AI compute commoditizes, Nebius’s margin expansion thesis requires that its long-term contracts remain priced favorably relative to future market rates, which is uncertain at multi-year durations.

Overall Risk Level: High

Valuation Context

Current stock price is approximately $95.65 (March 5, 2026 close) following Missouri campus approval, within a 52-week range of $18.31-$141.10 and approximately 32% below the October 2025 peak of $141.10. The stock has declined recently after CoreWeave’s post-earnings selloff on February 27.

The trailing EV/Sales of approximately 42x reflects the same fundamental dynamic as before: you are paying for what this business will be rather than what it is today. On management’s 2026 guidance of $3.0-$3.4 billion revenue, the forward multiple at current prices compresses to approximately 6.5-7.4x. For a business growing at this rate with these margin dynamics, sub-7x forward revenue is a reasonable basis for analysis, particularly as CoreWeave’s post-earnings correction has compressed CRWV’s forward multiple to roughly 5-6x 2026 estimates — narrowing the premium Nebius carries relative to its larger peer.

Analyst Context: Average 12-month price target approximately $151 (range: $108-$232), implying approximately 58% upside from $95.65.

Market Opportunity & Risks Score: 19/30

INVESTMENT THESIS

Key Strengths

1. Hyperscaler Validation Confirms Engineering Moat

Microsoft’s $17.4–$19.4 billion five-year contract and Meta’s $3 billion commitment together establish Nebius not as a commodity capacity rental business but as a technical partner trusted by the world’s largest AI spenders. Azure has essentially unlimited capital to build its own compute infrastructure, yet chose to purchase GPU capacity from an eighteen-month-old neocloud because Nebius could deliver training performance at scale that Azure could not guarantee internally. That validation commands durable pricing power, creates multi-year revenue visibility, and is the most credible third-party signal available that the engineering differentiation argument is real rather than marketing.

2. Contracted Power Pipeline Creates a Multi-Year Competitive Buffer

Nebius’s 2+ GW of contracted power, targeting 3+ GW by year-end plus the newly approved 1.2 GW Missouri campus, constitute barriers that new entrants cannot replicate simply by outspending. Permitting, grid interconnection negotiations, and construction take 18–36 months regardless of available capital, giving Nebius meaningful protection from well-capitalized competition over the relevant investment horizon. Combined with custom server chassis and networking software that commodity GPU resellers cannot match, this infrastructure position is the clearest near-term moat the business has.

Key Concerns

1. Microsoft Concentration Is Binary Risk

A single customer currently represents more than 80% of contracted 2026 backlog, meaning any disruption to the Microsoft relationship would not merely slow growth but eliminate the basis for the entire 2026 thesis simultaneously across revenue, CapEx justification, debt serviceability, and investor confidence. Meta’s $3 billion commitment is meaningful progress, but until non-hyperscaler enterprise revenue becomes a material share of the total, Nebius operates with a single point of failure that no engineering capability can offset.

2. Execution at This Speed and Scale Has No Proven Track Record

Nebius is attempting a 4–5x expansion in connected capacity within a single calendar year, across three continents, with $15+ billion in CapEx, and CoreWeave’s Q4 2025 earnings miss shows exactly how these situations fail and how severely the market prices that failure. NVIDIA Blackwell availability is constrained, construction requires regulatory approvals across multiple jurisdictions, and even a six-month delay in New Jersey would call the entire 2026 ARR guidance into question while potentially creating liquidity stress.

Bull Case

In the bull scenario, Nebius’s buildout proceeds largely on schedule. Connected capacity reaches 800 MW–1 GW by year-end, Microsoft and Meta capacity comes online as contracted, and ARR exits 2026 at the high end of the $7–$9 billion target. Revenue lands near $3.2–$3.4 billion with adjusted EBITDA margins approaching 40%, generating over $1 billion in adjusted EBITDA and transforming the investment narrative from pre-profitability land-grab to scaled AI infrastructure platform.

Marc Boroditsky’s enterprise sales effort gains traction, AI Cloud 3.1’s regulated-industry certifications open healthcare and financial services verticals, and non-hyperscaler enterprise revenue grows to represent a meaningful share of the total, thus reducing the Microsoft dependency that currently constrains the multiple. As the $20+ billion backlog converts into recognized revenue and the business approaches cash flow breakeven, the addressable investor base expands from speculative growth funds to quality-growth and infrastructure-focused institutions, supporting a durable re-rating.

Bear Case

In the bear scenario, at least one major 2026 buildout project encounters a meaningful delay. A data center partner falls behind in New Jersey, Blackwell allocation is redirected by NVIDIA to a higher-priority customer, or a European regulatory approval takes longer than planned. The delay does not need to be a cancellation to be damaging. A Nebius guidance cut at current valuation levels would likely produce a comparable or worse reaction, as the stock prices in flawless execution with no cushion for slippage.

Each compounding concern (revised ARR target, questioned debt facility, potential dilutive raise) reinforces the others, and if hyperscalers accelerate in-house AI compute buildouts through 2027–2028, the pipeline of multi-billion neocloud contracts that sustained Nebius’s ramp may not repeat at sufficient scale after the Microsoft buildout completes, leaving the company with extraordinary infrastructure assets and insufficient demand to fill them at premium pricing.

Valuation Assessment

Making an objective valuation for Nebius is not straightforward. I created a revenue model based on contracted power between 2026 and 2029 considering Microsoft and Meta deals + other customers. The company stated in the last earnings call that they expect revenue to be around $3.2B in 2026, with an mid-point ARR of around $8B, which I remind people it is the last month of the period in consideration x 12, which in this case implies around $666M per month. Let’s remember that ARR is the conversion from power to $ that the company expects to be contracted for, and therefore, not yet connected and producing revenue.

To reach the revenue expected by the company in 2026, in a base case scenario, one should assume that at least 70% of the capacity needed to fully serve the Microsoft deal for one year will be available and producing revenue. This is not an easy assumption, as it would mean that Nebius will be able to very quickly connect the needed capacity. With this assumption, Microsoft would make up around 76% of the total revenue, with 18% coming from the Meta deal, and the remaining 6% from smaller customers that use a mix of GPU-as-a-service and the Nebius software stack.

I assumed that the Microsoft and Meta deals both are paid at $2.7 per GPU-hour, with a hourly energy consumption for the full connection of presumably NVIDIA GB300 GPUs (GPU + network + IT + facility overhead) of 2,300 W (per GPU). This means that for the £2.436B in 2026 from the Microsoft deal ($17.4B / 5 * 0.7), there would be 102,993 GPUs employed (revenue / $-hour/ 8,760 hours in a year), with a total consumption of 237MW. With the same calculation, on a revenue of $580M from the Meta deal, there would be 24,522 GPU used, or 56MW. For the remainder smaller customer I assumed a $6 GPU hourly cost and a 2,000W consumption, assuming the use of older NVIDIA chips. This would mean using around 3,501 GPUs, or 7MW, with a revenue of $184M.

Let’s make it clear that a $3.2B revenue in 2026 for Nebius would mean a 504% increase YoY, which is huge. Assuming steady gross margin, decreasing OpEx fraction, and increasing net debt (total cash - total debt), with an EV/Sales between 15 and 17 (practically a third of what it is now), the price (on paper) should range between $170 and $195 at the end of 2026. For Nebius stock price to keep rising, Nebius MUST announce other hyperscaler deals, otherwise its growth would primarily come from an increasing smaller customer base. Even assuming a growth of this of 40% per year, while the CAGR in 2027 will be between 30% and 43%, it would contract (be negative) in 2028 and 2029.

If Nebius does announce a new hyperscaler deal, assuming this gradually increases up to 2029, and covering 40% of revenue, the CAGR for 2029 would be 16-25%.

Valuation Assessment: 4/10

FINAL VERDICT

Research Quality Assessment

My 58/100 research quality score reflects a business with genuine competitive advantages in an extraordinary growth market that is simultaneously carrying risks that are existential in character rather than merely financial. The competitive position score of 18/30 captures a company with real moats (technical differentiation, contracted power, NVIDIA partnership) that are not yet durable enough to qualify as wide-moat given commoditization risk. The business quality score of 17/30 reflects a trajectory that is genuinely impressive but pre-profitability with extreme capital intensity. The market opportunity score of 19/30 acknowledges a large and growing TAM against risks that could impair the thesis without warning. The valuation assessment score of 4/10 reflects not only the challenge of modelling Nebius revenue but also recognition that Nebius must announce other hyperscaler deals to justify future stock price and revenue targets.

The Trade-Off

Investing in Nebius means accepting binary customer concentration risk and unprecedented execution demands in exchange for exposure to what may be the fastest-scaling infrastructure business in modern technology history. On the positive side, you get hyperscaler-validated engineering quality, a $20+ billion contractual backlog, and a margin trajectory that points toward a highly cash-generative business within 12-18 months if execution holds. On the risk side, you give up predictability: a single relationship disruption, construction delay, or hyperscaler strategic shift could materially impair the thesis, and the valuation leaves no cushion for such an outcome.

Investor Fit

Nebius suits investors with high risk tolerance, a 3-5 year investment horizon, and genuine conviction in the structural AI infrastructure demand cycle. The volatility profile is extreme, the ATM equity program creates dilution overhang, and the customer concentration means the stock will respond violently to any news that questions the 2026 buildout schedule.

The research quality score 58/100 shows me that the mix of factors outlined in this deep-dive make investing in this company highly risky. This is a typical high-risk, high-reward setup, and investing in Nebius today means that you trust that the company will execute flawlessly in the next few years, and that new deals will start popping up left and right.

Valuation Conclusion

I understand the revenue model I outlined above is hard to digest in one go, and I am happy to share my actual revenue model should you wish to see it. However, this goes to show that not only predicting what Nebius revenue will be in the future is challenging, but also extremely uncertain. As things stand, once could only ‘reliably’ project revenue up to 2027, with subsequent year showing negative CAGR with the current deals only. I have no doubt that the company will announce other deals in the comping month, but their scale and timing will be fundamental to determine where the price could go.

Disclaimer

This newsletter is for educational and informational purposes only. Nothing I write constitutes financial advice, investment recommendations, or a solicitation to buy or sell any securities. You should not make investment decisions based solely on my analysis. Always do your own due diligence, consult with qualified financial advisors, and consider your individual circumstances before making any investment. All analysis and opinions are my own and can be wrong. Markets are uncertain, and even well-researched ideas can lose money. I am not a licensed financial advisor and accept no liability for any losses resulting from the use of information in this newsletter.